Loan Calculator: Simplify Your Loan Planning

Table of Contents

Introduction to Loan Calculators

Why Loan Calculators Are Essential

Understanding Loan Payments

The Importance of Loan Terms

Key Features of a Loan Calculator

Loan Amount & Interest Rate Input

Flexible Loan Term Options

Payment Frequency Choices

How to Use the Loan Calculator

Step-by-Step Guide to Calculate Loan Payments

Analyzing the Results

Benefits of Using a Loan Calculator

Simplifies Financial Planning

Helps You Compare Loan Options

Loan Calculator for Mortgages and Other Loans

Mortgage Calculations Made Easy

Car Loans, Personal Loans, and More

Loan Comparison: Choosing the Best Option

Comparing Loan Terms and Interest Rates

Impact of Extra Payments on Your Loan

Conclusion: Why You Need a Loan Calculator

FAQs

Introduction to Loan Calculators

When it comes to borrowing money, understanding the costs involved is essential. Whether you’re purchasing a house, car, or funding personal projects, loans are often necessary for making big purchases. But how do you know if you’re getting the best deal? How do you calculate what you’ll owe each month, or how much interest you’ll pay? The answer lies in a Loan Calculator.

A loan interest calculator allows you to estimate monthly payments, compare loan offers, and even figure out how much you’ll end up paying over the life of the loan. It simplifies the otherwise complex process of loan planning. With tools like a monthly payment calculator or a loan amount calculator, you can make more informed decisions about your finances and avoid costly surprises.

Key Takeaways

- Loan calculators help you estimate monthly payments, interest, and overall loan costs.

- They are essential for financial planning, whether you’re taking out a mortgage, car loan, or personal loan.

- A loan comparison tool enables you to compare different loan offers, making sure you get the best deal.

- Loan calculators save time and provide clarity, ensuring you’re financially prepared before making any commitments.

Why Loan Calculators Are Essential

Whether you’re applying for a home loan calculator or considering a personal loan, understanding the details of your loan terms is critical. Here’s why loan calculators are so helpful.

Understanding Loan Payments

One of the most important features of a loan term calculator is the ability to calculate your monthly payments. Knowing your monthly payment amount helps you determine if a loan fits within your budget. A loan amount calculator allows you to input your desired loan amount, interest rate, and term to figure out the payment you’ll make every month.

Understanding these payments in advance will give you peace of mind, as you can plan your finances accordingly and avoid being overwhelmed by debt.

The Importance of Loan Terms

The length of your loan term directly impacts the size of your monthly payments. A longer loan term might result in lower monthly payments, but you’ll pay more interest over time. Conversely, a shorter term results in higher payments but less interest in total. A loan interest calculator helps you weigh these options by providing detailed information about how the term and interest rate influence your payments.

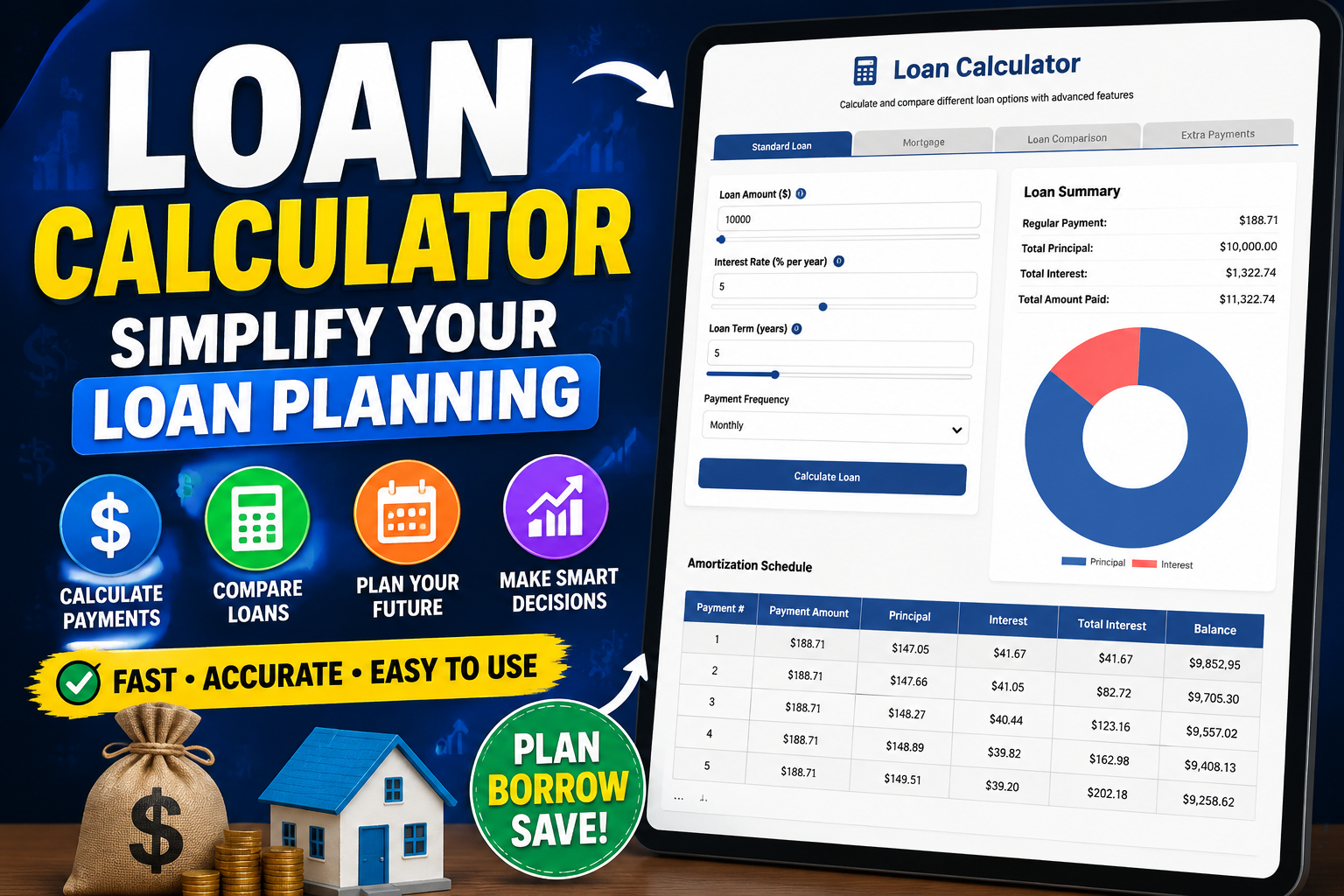

Key Features of a Loan Calculator

A Loan Calculator offers several important features to help you plan and manage your loans effectively. Let’s break down some key features.

Loan Amount & Interest Rate Input

Most loan calculators allow you to input the principal amount you’re borrowing, as well as the interest rate. The interest rate is a major factor in determining your monthly payments and the total cost of the loan. Having this information in one place makes it easy to see how much you will pay over the life of the loan.

Flexible Loan Term Options

You can also adjust the loan term—whether it’s 15 years for a mortgage or 5 years for a car loan. The loan term calculator helps you visualize how adjusting the term affects your monthly payments and total interest paid. It gives you a clear view of your financial obligations.

Payment Frequency Choices

Different loans might have different payment schedules—some require monthly payments, while others may allow bi-weekly or weekly payments. A loan comparison tool allows you to enter your preferred payment frequency, helping you understand how different payment intervals impact your budget and the total interest cost.

How to Use the Loan Calculator

Using a Loan Calculator is simple and can be done in just a few steps.

Step-by-Step Guide to Calculate Loan Payments

- Input your loan amount (the principal you are borrowing).

- Enter the interest rate—this could be fixed or variable, depending on your loan.

- Choose the loan term—how many years you plan to pay it off.

- Select your payment frequency—whether you’ll be making monthly, bi-weekly, or weekly payments.

- Click calculate to receive a breakdown of your monthly payments, total interest, and how the loan will be paid off over time.

Analyzing the Results

Once you’ve input all the necessary information, the calculator will provide you with a detailed breakdown of your loan. It will show you the monthly payments, total interest paid over the life of the loan, and how long it will take to repay the loan. This breakdown helps you understand the true cost of the loan and gives you the tools to make informed decisions.

Benefits of Using a Loan Calculator

Loan calculators aren’t just convenient—they come with a lot of benefits that make managing loans easier and more transparent.

Simplifies Financial Planning

A loan term calculator helps you plan your budget by showing you how much you’ll pay each month. By understanding your monthly payment obligations, you can allocate your finances more effectively and avoid surprises down the road.

Helps You Compare Loan Options

By inputting different loan offers, you can easily compare terms, interest rates, and monthly payments. A loan comparison tool allows you to visualize which option fits your budget and which loan is the best deal for your needs.

Loan Calculator for Mortgages and Other Loans

Loan calculators aren’t just useful for personal loans. They can also be a game-changer for mortgages and other types of loans.

Mortgage Calculations Made Easy

A home loan calculator helps you estimate how much you can afford to borrow and what your monthly mortgage payments will be. This is especially helpful when planning to buy a home and determining your affordability.

Car Loans, Personal Loans, and More

Whether you’re applying for a car loan or a personal loan, the loan amount calculator allows you to see your payment schedule and the total cost of the loan. It helps you make decisions based on your financial situation.

Loan Comparison: Choosing the Best Option

Comparing Loan Terms and Interest Rates

Using the loan comparison tool, you can analyze different loan offers side by side. This makes it easier to understand how different terms and interest rates will impact your overall cost and monthly payments.

Impact of Extra Payments on Your Loan

Many loan calculators allow you to see how making extra payments will shorten your loan term and reduce interest. This feature helps you save money and pay off your loan faster.

Conclusion: Why You Need a Loan Calculator

Whether you’re considering a mortgage, personal loan, or car loan, using a Loan Calculator is a smart way to understand your financial commitment. By inputting different variables like interest rate, loan amount, and loan term, you get a clear picture of how the loan will affect your budget. It helps you compare different loan offers, plan for monthly payments, and even pay off your loan faster by making extra payments.

A loan calculator is a must-have tool for anyone taking out a loan—it’s a simple way to take control of your finances and avoid surprises.

FAQs

What is a Loan Calculator?

A Loan Calculator is an online tool that helps you calculate monthly payments, total interest, and loan terms based on your loan amount, interest rate, and repayment period.

How does the Loan Calculator work?

It calculates your monthly payments based on the loan amount, interest rate, loan term, and payment frequency you enter.

Can I compare different loans with a Loan Calculator?

Yes, you can input different loan offers into a loan comparison tool to compare interest rates, terms, and payments.

What is a Loan Term Calculator?

A Loan Term Calculator helps you understand how different loan terms (e.g., 15 years or 30 years) affect your monthly payments and total loan cost.

Can I use the Loan Calculator for mortgages?

Yes, you can use a home loan calculator to estimate your monthly mortgage payments.

Do I need a Loan Calculator for car loans?

Yes, a loan amount calculator is perfect for estimating monthly payments for car loans.

What are extra payments, and how do they affect my loan?

Making extra payments reduces the principal balance faster, saving you money on interest and shortening the loan term.

Is the Loan Calculator free to use?

Yes, most loan calculators are free to use online.

Can I adjust the payment frequency on the Loan Calculator?

Yes, you can choose different payment frequencies, such as monthly, bi-weekly, or weekly.

How accurate are the results from a Loan Calculator?

The results are highly accurate as long as you input correct information regarding the loan amount, interest rate, and loan term.

Ready to calculate your loan payments?

Click here to use the Loan Calculator now!